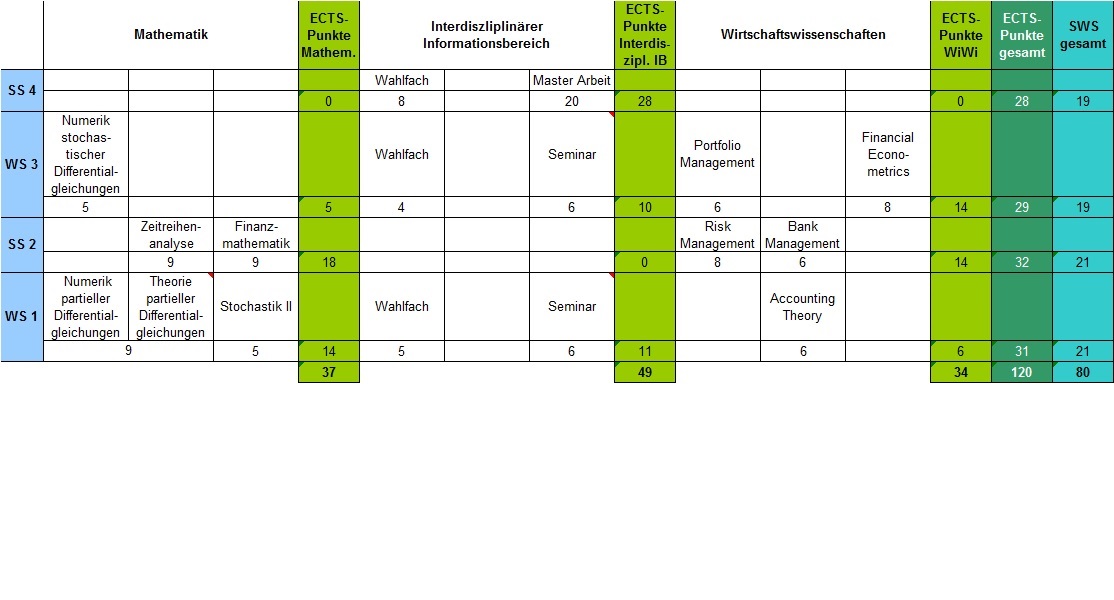

On this page, you will find an overview of the compulsory courses in the Master’s Programme in Mathematical Finance. In the first three semesters you will attend courses, meanwhile the fourth semester is to a large extent reserved for the master’s thesis.

New examination regulations from winter term 2023/24 onwards!

In the winter term 2023/24, new examination regulations will enter into force. Everybody starting the MSc Mathematical Finance from the summer semester 2023 onwards, will study with the new plan of study - have a look at it here.

Students already inscribed in the MSc Mathematical Finance will have the chance to change to the new plan of study. You may inform yourself on this website.

Important: The following information on this website refers to the examination regulations 2023, valid from 1 October 2023 onwards. If you started to study in this programme before the summer semester 2023 and haven't switched to the new plan of study, please inform yourself about the valid regulations for you by means of the examination regulations and the study plan 2017 (see beneath).

Mathematics modules

- Theory of partial differential equations

- Stochastical analysis

- Time series analysis

- Financial mathematics

- Numerics of stochastic differential equations

Economics modules

- Financial econometrics

- Bank management

- Financial reporting

- Portfolio management

- Risk management

Electives

You must collect a total of 22.5 ECTS credits in the electives. To do so, you can complete master’s courses in the Department of Economics as well as the Department of Mathematics and Statistics which are not covered by the other modules or choose courses from the Department of Computer and Information Science according to the course catalogue. The Standing Examination Committee can approve and announce other subjects.

Seminars

You will complete two seminars on the scale of 6 ECTS credits each, either offered by the Department of Mathematics and Statistics or by the Department of Economics.

{kind=link}